|

|

Are you buying?

Buying a property to live in rather than renting, has become more and more common in recent years as the availability of mortgages in general has increased. Below we have outlined what we feels are the 10 Steps you need to consider when home buying.

- You become aware as to whether buying a property is possible

- Establishes your borrowing potential so you know what properties are affordable

- See what purchase or selling costs are coming your way so there are no hidden surprises when you do find

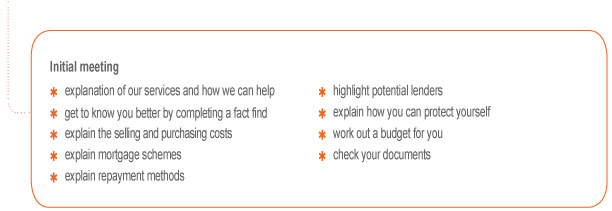

- Understand the five key decisions you need to make regarding; mortgage schemes, repayment methods, potential lenders, protecting yourself and suitable budget

- Get your documents such as passport, bank statements and payslips checked upfront - so there are no problems with paperwork when you do find a place

|

|

- Help’s establish your borrowing potential upfront so you know what properties you can afford to buy

- We issue you with a mortgage certificate so sellers and estate agents know you are in a good position to buy

- Speeds up your mortgage application later in the process as you have a credit check done upfront with a suitable lender

- Checks for any hidden credit problems before your consider looking for a property

- You become a Best Buy purchaser after we explain the five key decisions, issue a mortgage certificate, check your paperwork and pre-instruct a solicitor for when you find

|

|

- List your exact requirements so you only view suitable properties

- Consider your location for work, family, transport links, shops, amenities, socialising, local services or any other important factors?

- Consider the type of property to suit your needs i.e. house or flat, style of property, number of rooms required, what floor you prefer the property on, whether you need outside space?

- Go and view a property if you feel it meets your requirements by making an appointment with the estate agent, or seller direct if being sold privately

- On the first viewing look out for any obvious signs of damage and don’t be sidetracked just looking at superficial features like colour or furnishings. Consider taking a friend who may spot something you miss, and discuss any defects with the owner

- If you like the property then it is important to visit the property again, but be more methodical this time - taking notes if need be. You may want to consider visiting at a different time of day as areas can change

- Ask the owner or estate agent to confirm the properties running costs. These may include council tax, service charges, ground rent etc... If these are higher than expected, then these could affect affordability

|

|

- If you like the property then put in an offer straight away. Don’t be afraid to offer well below the asking price, as it may be accepted and save you a lot of money. Many sellers will market their property at a higher price expecting a lower price to be agreed in any case

- If you agree a price then make sure it is on condition that the seller takes the house of the market, so you are not gazumped (when another buyer comes in with a higher offer once the sale is agreed)

- If there is anything that you would like the seller to leave behind in the property then make sure this is included in the “agreed price” at this stage

- Negotiate the “sale being subject to survey and contract” as this allows you to withdraw from the purchase should there be any issue with these matters. If the seller insists on a deposit, or tries to limit timescales for purchase, then bring this to our attention

|

|

- Next you need to find a solicitor, or a licensed conveyance to begin the legal paperwork, and you should provide these details to the seller asap. If you’re not sure who to use, then ask us to recommend someone if you are not a Best Buy purchaser already

- Conveyancing is the process of transferring the legal ownership of properties between people, and your solicitor will aim to check the legal aspects of the sale after receiving a “draft contract” from the seller’s solicitor for approval

- The solicitor will look to confirm whether the seller has the legal right to sell the property, that no one has right of way over it, and that there are no land disputes. Your solicitor will check the local authority searches, and other information detailed in home information packs

- If there any concerns your solicitor has, then they may raise “preliminary enquiries” with the seller’s solicitor to clarify. As more information is received regarding the property through the result of your solicitor’s checks then “further enquiries” maybe raised.

- Once results of the local authority searches and answers to the preliminary/further enquires are received, the draft contract is approved by your solicitor, providing there nothing outstanding and a report is sent to you detailing their findings

- Check your five key decisions relating to mortgage schemes, repayment methods, suitable lender’s, protecting yourself and monthly budget haven’t changed from when they were first discussed

- Your mortgage agreement in principle is re-checked to see if it’s still with the most suitable lender for your needs, or we will look to advise you of alternative options by searching the “a comprehensive panel of lenders” again, and possibly carry out another credit check elsewhere

- If you already have a mortgage then it is worth considering whether it’s best to transfer this across to the new property, rather than look for a new lender altogether

- Complete your mortgage application as a priority, pay all fees and ensure any suitable documentation is ready - to fulfil chosen lender’s criteria. This can be completed face to face, or over the phone to save time

- During the mortgage application process the basic valuation, homebuyers or full building survey are instructed. The mortgage company will insist on a basic valuation as a minimum to check the price you are paying for the property is realistic

- Basic Valuation - Surveyor puts a notional value - in their opinion - on the value of your new home which determines the value. It may not spot any major faults however, but is the cheapest option and some lenders provide this free

- Homebuyer Survey – Surveyor spends more time in property and is more thorough, highlighting any serious defects. It will be more expensive, but it can end up saving you money if any major faults are highlighted - meaning you go back and renegotiate the price.

- Full Building Survey - Surveyor details the condition of your property in even greater depth, and more suited to older properties or unusual construction types. It costs more than a homebuyer’s survey and raises a lot of technical points, which may require further discussion with the surveyor

- Complete your mortgage application and finalise your protection arrangements by discussing any concerns you may have if your personal, or families circumstances were to change

- You will receive a Suitability Letter confirming what applications you have made and this provides an opportunity to double check all arrangements are correct

|

|

- This document states that the lender is prepared to offer a mortgage for the purchase of a property if your basic valuation and supporting documentation are satisfactory. This document will give details on the exact amount of money that will be lent to you and on what terms

- The mortgage offer will be sent to you and your solicitor directly by the lender to be checked. Certain lenders will ask you to carefully check through and sign a copy for return – always consult your mortgage consultant or solicitor at this stage. Once signed and returned your mortgage is in place and you are ready to exchange contracts

|

|

- Double check you are still happy with the property/mortgage/protection arrangements because once contracts have been exchanged with the seller. You will be financially liable if you pull out for any reason - it is important to be fully committed at this stage

- You normally commit 10% of the purchase price to the seller at this stage from your deposit - which is forfeited if you pull out

- Contracts are exchanged between you and the seller - a process carried out by solicitors on your behalf. Both parties will be committed to the deal at this stage, and a signed contract will have been signed by you and the seller enabling this to happen

- At exchange of contracts you are also responsible for insuring the property for buildings cover with the lenders interest noted on the insurance policy. This is most likely when purchasing a freehold property, rather than a leasehold place

- The seller at this stage is also bound by the “contract” and cannot accept a higher offer. This is also when the completion date is set for when you pick up the keys and move in

- Normally occurs within 1-2 weeks of contracts exchanging, and is the day your mortgage lender sends the remaining funds to your solicitor. Your solicitor will then transfer the funds to the seller's solicitor - alongside your deposit - so you have fully paid for your new home

- If you are moving home then your solicitor will arrange for your existing mortgage - if you have one - to be paid off at this stage. If you are transferring your existing mortgage to the new property then the solicitor will request funds from your current lender

Are You Remortgaging?

In recent years remortgaging has become much more common as the mortgage market becomes competitive and lenders pay for any transfer costs - not just for residential mortgages, but buy-to-let as well. People tend to switch lenders every few years now in order to reduce their monthly payments, or simply to release equity.

When remortgaging it is important to consider how the process actually works and we have detailed the 5 Steps to consider.

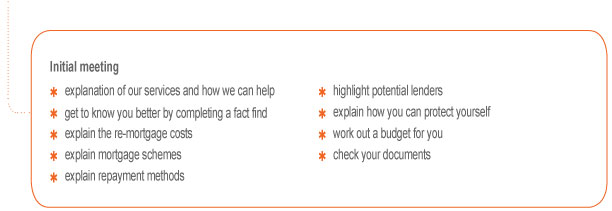

- Before you decide to remortgage it is important to consider the details of your current mortgage arrangements and evaluating its competitiveness within the marketplace. Consider whether completing a remortgage is necessary

- Understand what remortgage costs are coming your way so there are no hidden surprises from your existing or new lender. Even if monthly payments are lower is it still worth switching if the overall costs outweigh this benefit?

- Even if the total costs of remortgaging outweigh the benefits of staying with your existing lender then you may still choose to apply if your main priority is to cut your monthly payments, are experiencing problems borrowing extra from your current provider, or your current lender does not fulfil “other” important factors

- Establish your borrowing potential so you know what new lenders and rates are available if you decide to switch

- Understand the five key decisions you need to make regarding; mortgage schemes, repayment methods, potential lenders, protecting yourself and suitable budget

- Get your documents such as passport, bank statements and payslips checked upfront - so there are no problems with paperwork if you decide to apply

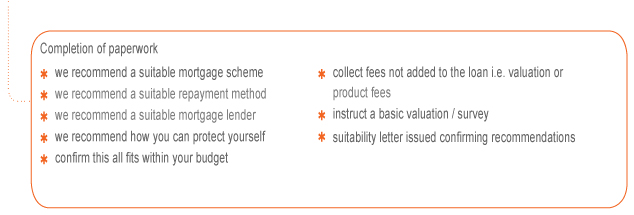

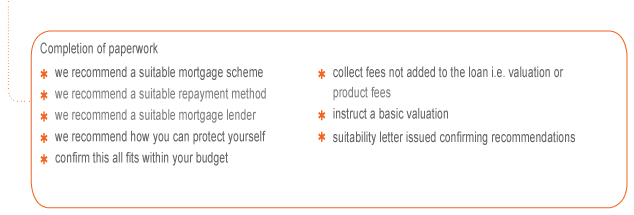

- Check your five key decisions relating to mortgage schemes, repayment methods, suitable lender’s, protecting yourself and monthly budget haven’t changed from when they were first discussed

- Carry out a credit check with what we recommend to be a suitable lender to meet your needs

- Complete your remortgage application if credit check passed, pay all fees and ensure any suitable documentation is ready - to fulfil chosen lender’s criteria. This can be completed face to face, or over the phone to save time

- During the remortgage application process a basic valuation is instructed as the value of your property will need to be re-assessed. The mortgage company will insist on a basic valuation as a minimum to check the value you are stating for your property is realistic, and normally this is at no cost to yourself

1. Basic Valuation - Surveyor puts a notional value - in their opinion - on the value of your current home which determines the value for remortgage purposes. Mortgage companies may choose to send a surveyor to your property, inspect from outside only, or use an indexed valuation at this stage

- Complete your mortgage application and finalise your protection arrangements by discussing any concerns you may have if your personal, or families circumstances were to change

- Mortgage companies will typically instruct a fees free solicitor or licensed conveyancer, working on their behalf, to issue a simple remortgage questionnaire to you at this stage. You may choose to use your own solicitor at this stage but this could be at your own cost

- You will receive a Suitability Letter confirming what applications you have made and this provides an opportunity to double check all arrangements are correct

|

|

- This document states that the lender is prepared to offer a mortgage for your property if the basic valuation and supporting documentation are satisfactory. This document will give details on the exact amount of money that will be lent you and on what terms

- The mortgage offer will be sent directly by the lender to you and the solicitors chosen to be checked. Certain lenders will ask you to carefully check through and sign a copy for return – always consult your mortgage consultant or solicitor at this stage. Once signed and returned your mortgage is in place and you are ready to move towards completion

-

Normally occurs within 1-2 weeks of mortgage offer being issued by your new lender

-

Conveyancing work needs to be carried out as this is the legal process of transferring ownership of the property. This involves switching the interests in your property between lenders only as the property will already be registered in your name.

-

During the conveyancing process, the formal mortgage offer will be checked, local searches will be conducted and a report and title sent to the new lender for their approval.

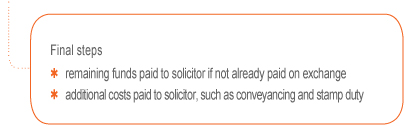

- If everything is satisfactory then your solicitor will ensure that your previous lender is repaid fully when the new lender releases mortgage funds.

- If you are borrowing less than your current mortgage outstanding, then your solicitor will request you pay them the shortfall at this stage. If you're borrowing additional funds, the solicitor will release these to you on completion

Buy to Lets?

Most Buy-to-Let Mortgages are not regulated by the Financial Conduct Authority.

Buying property for investment has become big business since the 1990’s, with many mainstream and specialist lenders keen to offer loans into this relatively new market. For many rental income has seemed attractive compared with what you could earn on other investments.

Apart from the traditional buying or remortgaging steps it is important to consider these additional 4 factors when considering buy to let investments.

When remortgaging it is important to consider how the process actually works and we have detailed the 5 Steps to consider.

|

|

-

Most lenders traditionally lend up to 85% of the property price or valuation, however 75% borrowing is more common in today’s market as a maximum. With residential mortgages, loans of 100% plus have been common in the past

-

Unlike residential mortgages where your income is used in determining how much can be borrowed. Buy to lets look at how much potential or actual rent is received on a property, and as a rule the rental income should be between 125-150% of the new mortgage payment

- Most lenders only require you to earn a minimum amount per year to be eligible, and some have no minimum income requirements at all. Most lenders do not restrict how many buy to let mortgages you can have in total as long as the rental income is sufficient

- Some lenders will only accept applicants with an existing mortgage, be it on a buy to let or residential basis. Accepting people with recent experience of paying mortgages generally excludes first time buyers from this market

- Remember that buy-to-let mortgages are not regulated by the Financial Conduct Authority in the same way traditional home loans are controlled. This means buy-to-let lenders do not have to follow strict rules on how they sell, promote and advertise their deals

-

Buy-to-let mortgages are likely to be more expensive than ordinary residential loans, and rates have been increasing in recent years as the property market has faltered.

- Buy to let mortgages will typically request that you make a 25% deposit/equity available if you want to purchase a new property, or remortgage an existing place

- Fees are broadly in line with those on conventional mortgages with regards to valuation and legal costs, but higher arrangement fees are common

- Associated costs, such as letting agent fees, accountancy fees and maintaining mortgage payments when the property is un-let are additional costs.

- Costs generally experienced by homeowners, such as insurance costs, ground rent, service charges and maintenance costs still apply. However, depending on your agreement with tenants you may not be liable for all typical household bills

|

|

-

The location, property type and condition are the three most important factors to consider when choosing a successful buy to let investment - good research is vital. Ask a few local agents for advice on what people are looking to rent locally and tailor these requirements to the property itself

- Don’t be side-tracked by your own preferences and consider what tenants are looking for instead. Factors such as transport, local schools, shops or socialising may be more important for your prospective tenants, but of little importance to you

- Consider paying extra for a property in good condition, unless you have the time and resources to refurbish something rundown.

- Most tenants are likely to require modern bathrooms, kitchens, and decor nowadays. Even though you can let your property on a furnished or unfurnished basis, most tenants require showers, fridges and washing machines as standard nowadays

|

|

-

You are allowed to offset interest payments from your mortgage against the tax liable on the rental income, along with other expenses such as letting agents fees, property maintenance costs and general running costs.

- The rental profit after costs have been deducted, will be treated as normal income and taxed in line with your basic or higher-rate tax bands. Therefore you may find yourself pushed into a higher rate tax band as a result, once rental profit is taken into consideration.

- Any increase in your property’s value could also be liable for Capital Gains Tax when you come to sell your property. Second homes, including buy to let, are liable for taxation whereas your main residence is exempt from this tax.

Thinkofmortgages.Com is a trading name of Thinkofmortgages Ltd who are an Appointed Representative of PRIMIS Mortgage Network, a trading name of Personal Touch Financial Services Ltd. Personal Touch Financial Services Ltd is authorised and regulated by the Financial Conduct Authority.

We may charge you a fee for mortgage advice. The exact amount will depend on your needs and circumstances. Our typical fee is £399.

|

|

|

|