|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||

| | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

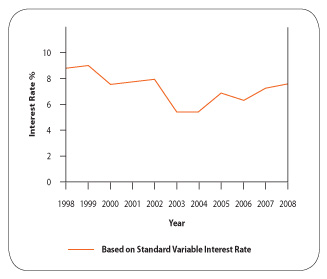

Standard variable rate

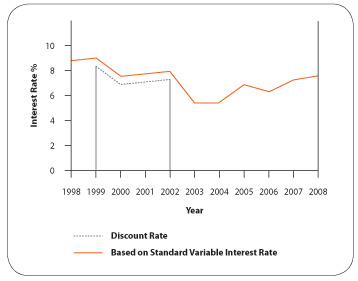

Discounted rate

Tracker rates

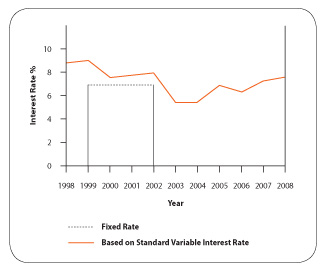

Fixed rates

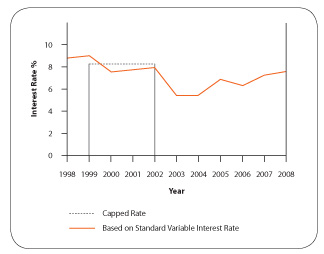

Capped rates

Collared rates

Your monthly payments can vary and this type of mortgage is typically used in conjunction with a capped rate or a tracker rate (see above). Your monthly payments are variable but will not fall below a set lower level (the 'collar'). Flexible mortgageYour monthly mortgage payments will tend to be higher on a flexible mortgage, but it gives you the scope to pay off your loan more quickly or to vary your monthly payments, suiting your ability to pay. Many flexible features are becoming more common in mainstream mortgage products and not just mortgages with 'flexible' in their name. The more common features are listed below:-

This type of mortgage is often combined with other mortgage schemes (i.e. fixed or tracker), and is more suited to those who have a variable income like the self-employed, or employed people receiving bonuses and commissions. If it is unlikely that you will use these flexible features, then a less flexible mortgage may be cheaper or more suited to your circumstances. Offset mortgageWith an offset mortgage you can find that your main current account or savings account (or both) become linked to your mortgage, even though held separately with the same bank or building society. You will find that each month the amount you owe on your mortgage is reduced by the balances in these separate accounts, before the interest due on your outstanding loan is worked out. You will find that as your current account and savings balances go up you pay less on your mortgage interest, and as they go down you pay more. This type of mortgage is often combined with other mortgage schemes (i.e. fixed or tracker), and is more suited to those who are looking to pay their mortgage off early. Most offset mortgage providers will maintain the same monthly mortgage payment even though interest rates or the loan may have reduced, effectively causing an “overpayment”. Some lenders will automatically adjust the payment to a lower level however, which doesn’t allow this “overpayment” to be created automatically. Current account mortgageA current account mortgage is similar to an offset mortgage in that it offsets the balance in your current account (savings) against your mortgage account (borrowings). In this case however, rather than your mortgage and current account being separate pots of money, they are usually combined into one account. This means that the combined account acts like one big overdraft against your property. This type of mortgage is often combined with other mortgage schemes (i.e. fixed or tracker), and is more suited to those who like to manage their finances in one place. Mortgage current accounts normally provide all the normal services associated with current accounts like a cheque book, access to cash machines and direct debit facilities. If you have substantial savings and you like the flexibility to make overpayments and underpayments when you choose, then you will find these attractive. If you have less savings overall then other mortgage schemes (i.e. standard fixed or tracker schemes) maybe more cost effective. Cashback mortgageYour monthly payments maybe higher on this type of mortgage, but you are compensated by the lender paying you a substantial sum (cashback) shortly after the loan has started. This can be a percentage of the loan amount, typically between 2-5% of borrowings - or a fixed amount. If you choose to move to another lender in the early years, most lenders will ask you to repay some or all of the cashback received. This type of mortgage can be combined with all types of regular mortgage schemes, and maybe suitable for those who require the cashback to cover any costs that may arise early on (i.e. legal costs or furnishings). If the cashback compensates for the fact that monthly payments are higher, then it may be considered for this reason also in isolation. Those who can forego the cashback now however, will normally get a better overall deal by selecting a different mortgage scheme option. Adverse credit mortgagesYour monthly payments will be higher on this type of mortgage and is typically available with all mortgage schemes (i.e. fixed or tracker). These mortgages are often described as non-conforming, sub-prime or adverse credit mortgages. They are suitable for those people who have had past problems, or are still encountering problems with their credit conduct.

Some of the above services may not be regulated by the Financial Conduct Authority YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE We may charge you a fee for mortgage advice. The exact amount will depend on your needs and circumstances. Our typical fee is £399

© 2023 Think of mortgages.com | terms & conditions | sitemap | privacy notice |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||